ISA vs Roth IRA - Are They the Same?

ISA vs Roth IRA: What US Expats in the UK Need to Know

Why a simple comparison can be misleading for cross-border planning

If you’re moving between the US and the UK, it’s natural to compare familiar investment accounts.

A common question is:

“Is a UK ISA the same as a Roth IRA?”

On the surface, they look similar. Both are designed to provide tax-efficient investment growth.

But for US citizens living in the UK, the reality is more complicated.

Understanding the differences, and how each is treated across both tax systems, is essential to avoid unexpected tax and planning issues.

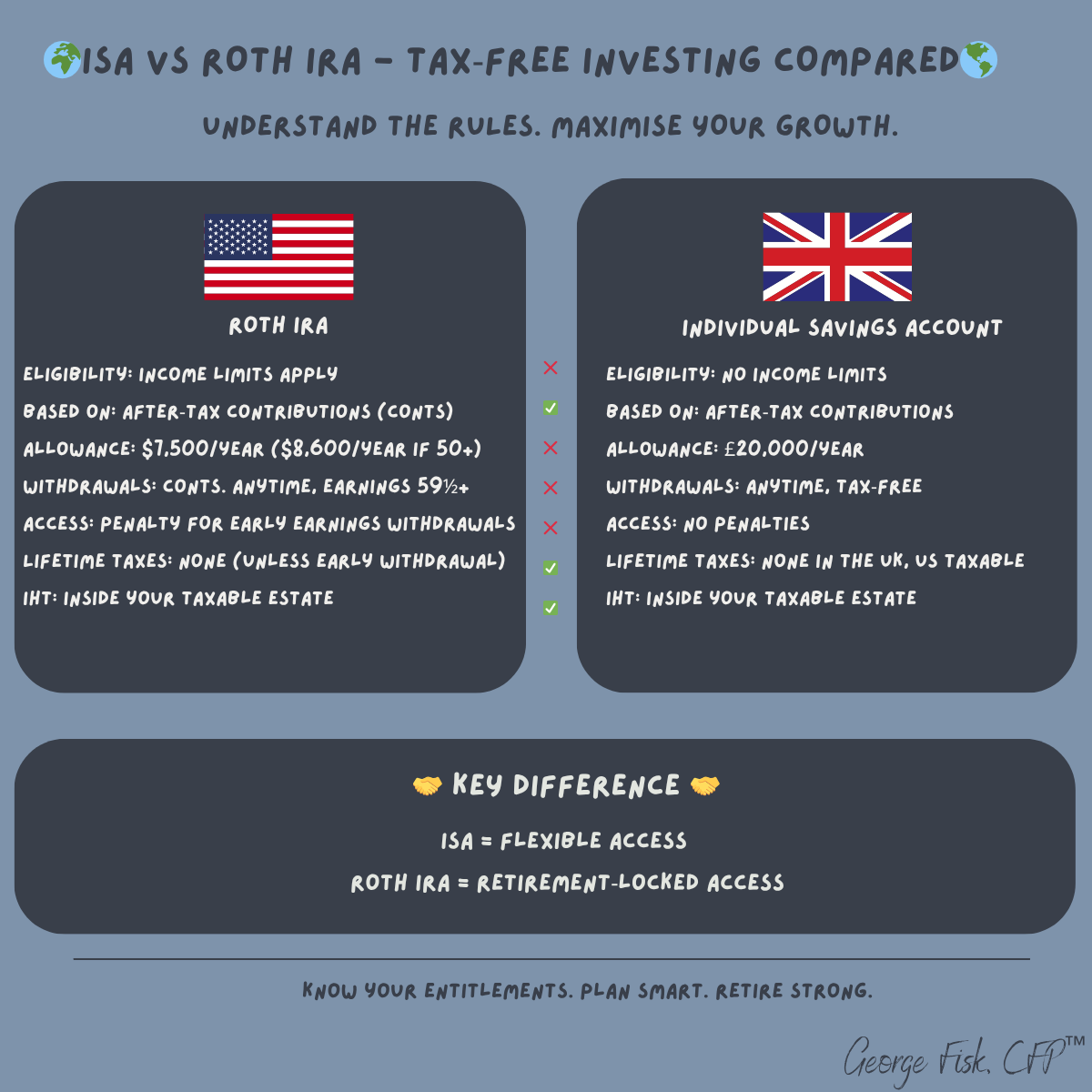

What is a Roth IRA?

A Roth IRA is a US retirement account funded with after-tax contributions.

Key features include:

Investments grow tax-free for US purposes

Withdrawals are tax-free in retirement (subject to rules)

Contributions are made from earned income

Annual contribution limits apply

For US residents, this is one of the most tax-efficient long-term investment structures available.

What is a UK ISA?

An Individual Savings Account (ISA) is a UK tax wrapper.

Key features include:

Investments grow free from UK income and capital gains tax

Withdrawals are tax-free in the UK

Annual contribution allowances apply

Flexible access (depending on ISA type)

For UK residents, ISAs are a core part of tax-efficient investing.

The key issue: they are not equivalent across borders

While both accounts are tax-efficient in their home country, they are not treated equally in a cross-border context.

This is where problems arise for US expats living in the UK.

How Roth IRAs are treated in the UK

In many cases, Roth IRAs can retain favourable tax treatment in the UK, particularly where treaty provisions apply.

However, this is not always straightforward.

Considerations include:

whether contributions were made while UK resident

how the UK interprets the account under tax rules

the timing of withdrawals

Used correctly, a Roth IRA can remain a valuable part of a long-term plan, but it needs to be coordinated with UK tax rules.

How ISAs are treated for US citizens

This is where many expats are caught out.

While ISAs are tax-free in the UK:

They are not recognised as tax-efficient by the US.

This can mean:

income and gains inside the ISA may still be taxable in the US

additional reporting requirements

potential exposure to complex US fund rules

In some cases, holding certain investments within an ISA can create further complications.

Investment complications inside ISAs

For US citizens, investing within an ISA can trigger issues such as:

holding non-US funds that fall under US anti-deferral rules

complex tax reporting requirements

potentially unfavourable tax treatment

This means that while an ISA may look attractive from a UK perspective, it can be problematic when viewed through a US lens.

Which is better: ISA or Roth IRA?

There is no one-size-fits-all answer.

It depends on:

your tax residency

where your income is earned

your long-term plans (US vs UK retirement)

your existing accounts and assets

In general:

Roth IRAs can be highly effective if managed correctly within a cross-border plan

ISAs require more caution for US citizens, particularly in terms of investment selection and reporting

A joined-up approach is essential

The key takeaway is that these accounts should not be viewed in isolation.

Decisions about ISAs and Roth IRAs need to be made as part of a coordinated US–UK financial plan.

This includes:

understanding how each account is taxed in both countries

selecting appropriate underlying investments

aligning your strategy with long-term residency and retirement goals